What Is Asset Tokenization on Blockchain? A Complete Guide

Asset tokenization is one of the most discussed trends in today's financial industry, blockchain technology, and the digital economy in general. It promises to transform the way we understand ownership, access to capital, investing, and asset management. In simple terms, tokenization makes it possible to turn almost any asset — from an apartment in the city center to a barrel of oil or a music catalog — into a digital token on a blockchain that can be easily owned, divided, traded, and used as collateral.

In this guide, we'll break down what tokenization is, how it works on both the technical and legal levels, which types of assets are most commonly tokenized, what the key benefits and risks are, and why many experts believe tokenization will become the new standard for global capital markets.

1. Basic Definition of Asset Tokenization

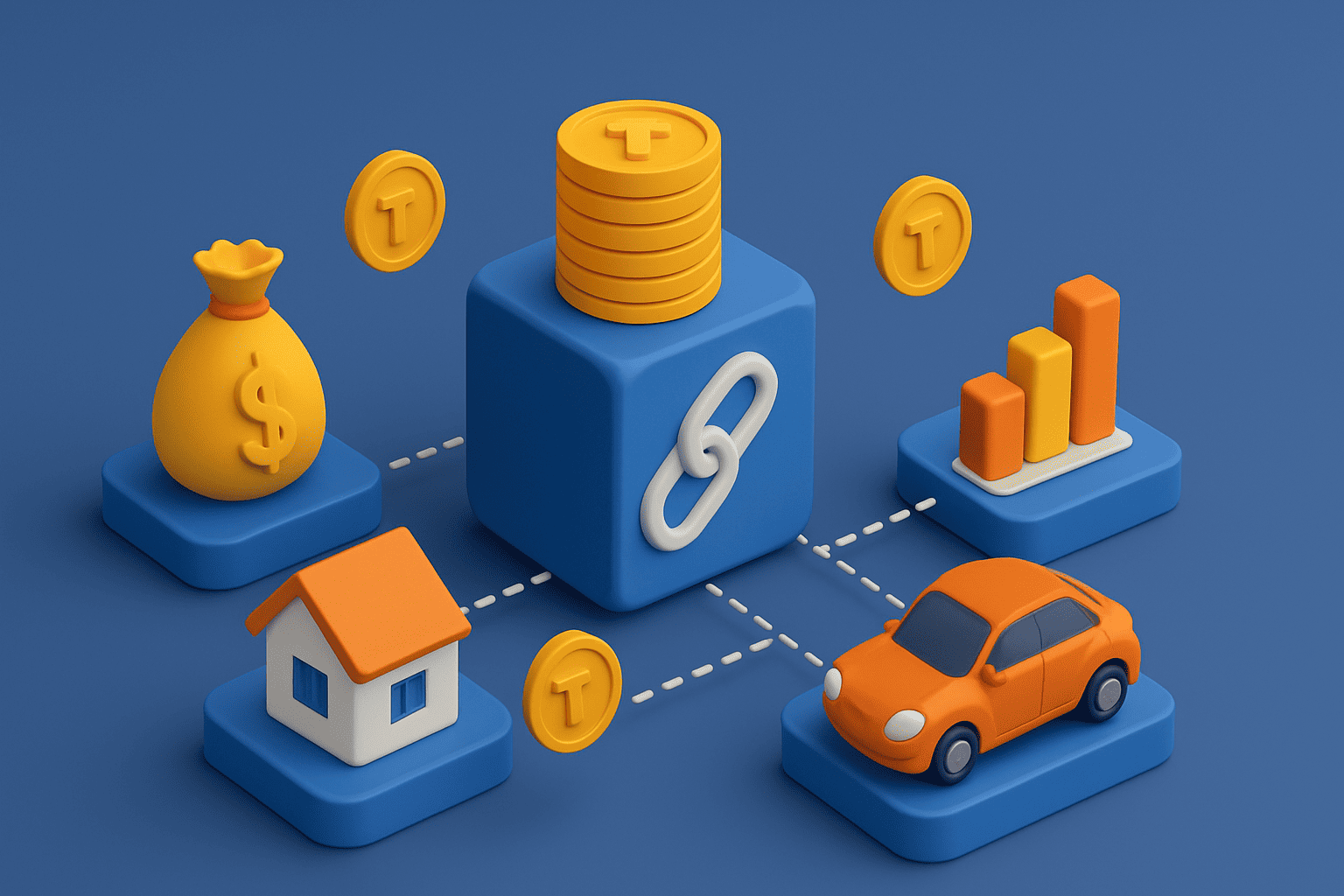

Asset tokenization is the process of creating a digital token on a blockchain that represents a real-world or digital asset (or rights to it). This token acts as a digital certificate that confirms:

- ownership of an asset in full or in part;

- the right to a share of income generated by the asset (for example, rent or royalties);

- the right to access certain products or services;

- other economic or legal rights tied to the asset.

In practice, this means we can take, for example, a house worth 500,000 USD and split it into 500,000 tokens, where each token corresponds to 1 USD of the asset's value. An investor who buys 5,000 tokens owns 1% of the house and is entitled to the corresponding share of the income generated by that property.

2. Why Has Tokenization Become So Relevant?

The traditional financial system often suffers from three key problems: limited access, complex procedures, and low liquidity for many types of assets. Expensive objects (real estate, art, infrastructure projects) are usually available only to large investors or institutions, and the process of buying or selling them can take weeks or months.

Tokenization addresses several challenges at once:

- Democratized access: fractional ownership lets people invest even small amounts into expensive assets;

- Global markets: tokens can be traded worldwide 24/7;

- Transparency: all transactions are recorded on a blockchain and can be verified;

- Automation: smart contracts reduce the role of intermediaries and bureaucracy;

- New monetization models: creators, businesses, and investors get new ways to interact.

3. Which Assets Can Be Tokenized?

One of the main questions for those new to the topic is: which assets are suitable for tokenization? The answer is: practically anything, as long as there is a legal way to structure the rights attached to the token.

Below is a summary table with the main asset categories and their specifics.

| Asset Category | Examples | How Tokenization Works in Practice |

|---|---|---|

| Real Estate | Apartments, office buildings, aparthotels, land | The property is split into a fixed number of tokens (e.g., 100,000), each representing a share of ownership and/or rights to rental income. |

| Financial Instruments | Stocks, bonds, mutual funds, private equity | Traditional securities are issued or mirrored in the form of tokens, allowing them to be traded on blockchain platforms and enabling automated dividend distributions. |

| Commodities | Gold, silver, oil, gas, other resources | Each token is pegged to a fixed quantity of a physical resource (for example, 1 token = 1 gram of gold) stored in a vault and redeemable under specific conditions. |

| Creative Assets & Intellectual Property | Paintings, music, films, patents, brands | The author or rights holder issues tokens representing a share of future royalties or income generated by commercial use of the asset. |

| Digital Assets | NFTs, domains, in-game items, digital collectibles | Unique tokens (most often in NFT format) represent ownership of a digital item that may exist entirely online. |

| Business Assets & Future Cash Flows | Equity in a business, future revenue streams, loan portfolios | Tokens are linked to specific contracts, cash flows, or an equity stake in a company; the investor receives rights to a share of profit or debt repayments. |

As the table shows, tokenization is not about a single market but rather a universal model of representing value that can be applied to many very different asset classes.

4. The Technical Mechanism of Tokenization: What Happens Under the Hood

While tokenization can look simple from the end user's point of view — “click a button and buy tokens” — there is a lot of technological and legal work happening in the background. We can roughly break it down into several stages.

4.1. Legal Preparation and Asset Structuring

The first step is to make sure that the asset is legally suitable for tokenization. This typically involves:

- legal due diligence of ownership rights;

- asset valuation (market value, expected yield, risks);

- defining which specific rights the token will represent (ownership, income, access, voting, etc.);

- creating a legal structure (SPV company, trust, fund, DAO, and so on).

It is crucial that the legal documentation clearly establishes: token = a specific right or share in the asset. Otherwise, the investor only receives a “marker on a blockchain” and not a real claim.

4.2. Smart Contract Development

A smart contract is a piece of code on a blockchain that defines the logic of how the token works:

- total supply (for example, 1,000,000 tokens);

- token standards (ERC-20, ERC-721, ERC-1155, SPL, etc.);

- rules for transferring, freezing, redeeming, and burning tokens;

- mechanisms for income distribution, voting, conversion;

- restrictions for specific categories of investors (KYC/AML, jurisdictions).

A smart contract runs autonomously: no one can arbitrarily change its logic after deployment to the blockchain (unless special upgrade mechanisms are built in from the start).

4.3. Token Minting and Initial Distribution

Once the smart contract is created, tokens are minted. They can:

- be allocated to founders and early investors;

- be sold via a tokenization platform or exchange;

- be issued as rewards or bonuses for participation in the project.

At this stage it is important that the token has a clear economic model: how many tokens are in circulation, whether new tokens can be issued in the future, how income is distributed, and which rights each investor has.

4.4. Secondary Market Trading

After the primary distribution, tokens can circulate freely on the secondary market — on exchanges, P2P platforms, or specialized marketplaces. This creates liquidity that traditional assets (especially real estate or private equity) often lack.

5. Types of Tokens in the Context of Asset Tokenization

Not all tokens are the same. In the context of asset tokenization, several core types are most commonly used, differing both in legal status and functionality.

5.1. Security Tokens

These are tokens that are legally treated as securities. They typically:

- represent an equity stake in a company, fund, property, or other asset;

- may entitle the holder to dividends or a share in profits;

- are subject to securities regulations (for example, SEC rules in the United States).

For such tokens, it is crucial to comply with regulatory requirements: KYC/AML, investor qualification rules, reporting standards, and so on.

5.2. Asset-Backed Tokens

In this case, the token is directly backed by a specific asset — for example, one ounce of gold, a barrel of oil, or a particular unit of goods. The token holder can usually:

- hold the token as a digital equivalent of the asset;

- sell the token on the market to another investor;

- redeem the token and receive the physical asset (according to platform rules).

5.3. Utility Tokens

These tokens do not necessarily represent the asset itself, but provide access to products, services, or functions within an ecosystem. They can be used:

- as an internal payment unit on a platform;

- to pay transaction fees;

- as a “ticket” into a particular service or membership club;

- for participation in governance or voting (governance tokens).

5.4. Non-Fungible Tokens (NFTs)

Non-fungible tokens (NFTs) are used for unique assets: artworks, music, collectibles, in-game items, and can also be used to certify ownership of a specific real-world object.

6. Benefits and Risks of Tokenization: Two Sides of the Same Coin

To fairly assess tokenization, it is important to understand not only its strengths but also its potential downsides. The table below summarizes the key advantages alongside the main risks and limitations.

| Aspect | Benefits of Tokenization | Potential Risks and Limitations |

|---|---|---|

| Access to Investments | Fractional ownership enables investing small amounts into high-value assets, opening markets to a broad range of retail participants. | Clear rules for retail investors are required; otherwise, there is a risk of misunderstanding the product and unrealistic expectations. |

| Liquidity | Tokens can often be sold much faster than traditional assets (for example, real estate), increasing portfolio flexibility. | In early stages, many tokenized assets may have limited demand, so liquidity can be more theoretical than real. |

| Transparency | All token transactions are recorded on a blockchain, improving trust and simplifying audits. | Blockchain transparency does not automatically guarantee issuer transparency: a project can still hide important details about the asset or corporate structure. |

| Automation | Smart contracts can automate payouts, conversions, and voting, reducing reliance on intermediaries and minimizing human error. | Bugs in smart contract code and unpatched vulnerabilities may lead to loss of funds or locked assets. |

| Regulation | Many jurisdictions are introducing clear regimes for digital assets, gradually making the market more mature and investor-friendly. | Regulatory uncertainty is still high; laws may change and introduce new restrictions or requirements for issuers and investors. |

| Technological Complexity | For advanced users, tokenization opens access to innovative instruments and the broader DeFi ecosystem. | For newcomers, dealing with crypto wallets, private keys, and blockchain platforms can be challenging, increasing the risk of mistakes and loss of access. |

7. Legal and Regulatory Aspects

No tokenization effort can be considered complete if it exists only “on the blockchain” but is not backed by proper legal foundations. For investors, the key question is: does the token have real legal force, or is it just a digital marker?

In practice, it is important to:

- clearly define in contracts which rights the token grants;

- understand whether the token is regulated as a security, commodity, or something else;

- ensure that the issuer complies with KYC/AML, investor protection, and reporting requirements;

- understand which jurisdiction the project operates in and what local digital asset laws apply.

Regulators around the world are moving toward formalizing the tokenized asset market, but approaches can differ significantly. This creates both opportunities (new licenses, regulatory sandboxes) and challenges.

8. Real-World Use Cases of Tokenization

Tokenization has long moved beyond theory and is actively used in various scenarios:

- Tokenized gold: tokens backed by physical gold stored in vaults allow investors to gain exposure to the metal without holding it themselves.

- Real estate: investors buy fractions of tokenized residential and commercial properties in different countries and receive proportional rental income.

- Tokenized funds: investment firms issue tokens representing shares in private equity or real estate funds, simplifying access for a wider range of investors.

- Music and creative royalties: artists and producers sell shares of future income in the form of tokens, raising capital directly from fans and investors.

- Metaverses and gaming: virtual land, items, and characters exist as tokens that can be owned, traded, and integrated into gameplay.

9. The Future of Tokenization: What to Expect in the Coming Years

Many experts believe that tokenization over the next 5–15 years could become a fundamental layer of the new financial infrastructure. It is expected that:

- more traditional financial instruments (stocks, bonds, funds) will be issued natively as tokens;

- real estate will increasingly adopt hybrid models where tokens are a standard tool for attracting capital;

- more regulated platforms will appear, bridging blockchain and traditional finance;

- governments may start tokenizing some of their assets or debt instruments;

- access to global investment opportunities will become as common as online banking is today.

10. Conclusion

Asset tokenization on blockchain is not just a buzzword or temporary hype. It is a deep structural shift that touches the very foundations of ownership, capital flows, financial services, and investment. It combines legal structures, blockchain technology, economic models, and new approaches to asset management.

For investors, tokenization opens access to new asset classes and allows for more flexible portfolio construction. For businesses, it is a tool to raise capital and improve liquidity. For the market as a whole, it is an opportunity to make the financial system more transparent, efficient, and inclusive.

That is why it makes sense to start understanding how tokenized assets work today, what risks and opportunities they bring, and what role they might play in your personal or corporate financial strategy in the years to come.